Aecon Group Inc

Aecon Group Inc

Government Services Oligopoly at 3x 2024 EBITDA, 5x FCF

Summary

We believe Aecon (TSX:ARE) has undergone a structural step-change in its MOAT trajectory and returns on incremental capital that is yet to be appreciated by the market. ARE is trading for only ~3x EBITDA our 2024 estimate with a ~5% dividend yield. Aecon's peers trade at 13-15x EV/NTM EBITDA. ARE trades at 8x our 2024 FCF estimate or 5x ignoring working capital.

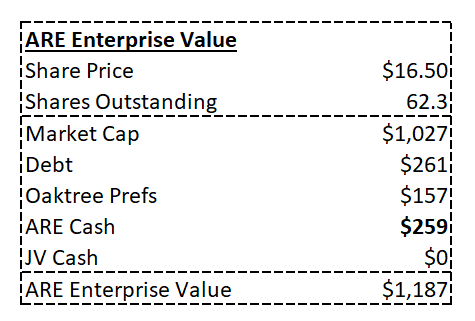

Net of Aecon's majority ownership of the Bermuda Airport and its standalone Utilities business, co-owned with Oaktree as of October 2023, ARE's remaining business are currently trading at an EV/EBITDA multiple of 1.8x.

Despite significant evidence to the contrary, current valuation suggests the market believes Aecon is a cyclical, low margin business with perpetual ongoing losses from legacy projects leading to greatly reduced earnings power.

We see Aecon as a high quality business with multi-year government contracts, a positive mix shift towards recurring revenues and a business producing accretive contribution margins paired with significantly reduced capital requirements.

Aecon is a government infrastructure services provider. Aecon provides infrastructure design, consulting, engineering and construction services to various federal, provincial/state and municipal governments across North America, primarily in Canada. End markets include projects focused on public transportation, environmental services, clean energy, and regulated utilities. Similar to other public-sector service providers, Aecon benefits from a customer profile with repeated purchase patterns, deep pockets, a lack of macro sensitivity, a preference to work with a small select group of service providers, and a disclosed multi-year backlog providing high visibility on future revenue.

ARE's competitive advantages includes decades of accumulated technical expertise and experience and the scale required to bid, design and complete large, multi-year projects. Aecon further benefits from a lengthy and extensive relationship with local governments allowing for security clearance and pre-approvals for RFPs.

Much like other industries offering a combination of higher/lower quality revenues with higher/lower margin profiles, the engineering and construction (E&C) industry has largely completed a multiyear mix shift towards higher quality engineering and design services and away from lower margin, commoditized construction revenues frequently associated with fixed-price contracts. These contracts place execution risk entirely on the construction builder such as Aecon with lumpy milestone payments requiring flawless execution to achieve profitability in line with the project's initial underwriting.

Unlike its E&C peers which have re-rated following the successful shift away from construction and fixed-price contracts, Aecon has been held-back by a combination of self-induced and macro-related headwinds that are now in the very final stages of dissipating. Going forward, Aecon has significantly reduced its sensitivity to large budget overruns that have historically led to a volatile earnings profile. We anticipate the market will place a much higher multiple on Aecon's underlying earnings power going forward.

Putting ARE's 2015-2019 average EV/EBITDA multiple of 6.5x our 2025 estimate produces a stock price of ~$36, nearly 2.5x Aecon's current share price and a >50% IRR. This multiple gives no credit for the quality improvement in Aecon's business, with a 2023 normalized EBITDA margin of >9% vs 4.5-5.5% historically from 2015-2019 while invested capital has been greatly reduced following two well executed asset sales. In our view this multiple also gives Aecon no credit for the reduced exposure to fixed-price contracts in Aecon's pro-forma backlog which will have gone from ~75% of the backlog pre-pandemic to ~25% at YE24.

Background

Aecon's origins date back to 1877, 10 years after the inception of Canada in 1867. Aecon has helped build some of Canada's most prominent infrastructure projects including Toronto's CN Tower, the Highway 407 Express, Vancouver Sky Train, and the Montreal-Trudeau International Airport.

In October 2017 Aecon was acquired by CCCC International Holding Limited (CCCCI), the state-owned engineering and construction arm of the Chinese government for $20.37 per share in cash, representing an enterprise value of $1.51 billion and ~9x NTM EBITDA relative to a $1.19 billion current EV and 3.4x our NTM EBITDA estimate. The deal was ultimately stopped in May 2018, with the federal government of Canada blocking the sale, citing national security concerns.

Recent Fixed-Price Contract Issues

From 2021-2023 Aecon has suffered from three years of project write-downs related to four low-margin fixed-price projects signed prior to the covid pandemic and the subsequent period of rapid inflation.

Aecon's four problem projects are the Windsor-Detroit Gordie Howe International Bridge, (2018, $5.7B), Toronto-based Finch West Light Rail Transit, (2018, $2.5B) and Eglinton Crosstown Light Rail Transit (2015, $5.3B) along iwth the Coastal GasLink Pipeline (2018, $526M) in BC.

These projects have led to substantial losses and depressed margins for Aecon which have masked the underlying earnings power and step change in the quality of the business. Not only are these fixed-price contracts, but that they are also very large multi-year mega projects that were particularly vulnerable to covid-related delays and cost inflation.

As a result, Aecon has written-down these projects by a combined $400M (2021: $66m 2022: $120m 2023: $215m), wiping out all expected profits from these projects and offsetting the majority of Aecon's earnings from its remaining portfolio of projects and its ownership of the Bermuda Airport.

All four legacy projects are now in the final stages of completion. The Coastal Gas Link, Eglinton LRT, and Finch West LRT projects are all either already complete or in the very final stages of technical construction while The Gordie Howe International Bridge, is now expected to be mechanically complete in September 2025 with technical construction completed in 2H24. The bridge is more than 2/3 finished with 140 meters (458 feet) remaining. The most difficult part of the project, installation of 722-foot towers is fully complete.

")

We estimate these four projects will account for only ~5% of 2024 revenue after accounting for 17% of revenue and a 60% reduction to normalized EBITDA in 2023. Going forward, Aecon's fixed price contracts will be limited to projects less than $1bn in size and account for only 1/4th of Aecon's pro-forma backlog.

As legacy projects approach completion, not only is Aecon's write-down cycle coming to an end, Aecon is likely to receive payment from its project partners for losses they've been forced to fully absorb but for which they are not at fault.

In Q4/23 Aecon received an undisclosed settlement from the Windsor Bridge Authority for shared cost overruns falling under a force majeure clause relating to the Gordie Howe Bridge. Fluor, ARE's JV partner on the bridge recognized a $69mn cash concession benefit from the project which would have translated to ~$47mn CAD for ARE if settlement's was based on propionate ownership of the project. Payments from project owners to E&C firms takes place if cost overruns fall under a category known as "shared risk". Language in ARE's disclosures suggests that Aecon's additional 3 fixed-price legacy projects all of which have taken loss write-downs for >100% of original profit estimates, also include shared risk clauses with cash payments to ARE likely occurring in the near term:

Aecon and its joint venture partners remain focused on dedicating all necessary resources to drive the four legacy projects to completion and in the meantime continue to pursue fair and reasonable settlement agreements with the respective clients in each case. Based on i) expected substantial completion achieved or expected to be achieved in the next twelve months on three of these projects as noted above; ii) the most recent settlements reached and agreed to between the relevant joint ventures and the respective clients on each of the four projects, including one in the second quarter and two in the third quarter of 2023; and iii) the adjustments to forecasts made on the legacy projects in the second and third quarters of 2023 that reflect the additional clarity on schedule, compensation, construction costs, and other potential liabilities that the terms of the most recent settlement agreements and full reforecasts that incorporate those agreements and other new information that has arisen bring.

In response to these problem projects, management has made it an emphasis to not sign fixed-price contracts above $1B. This is evidenced by the fact that both the Go Expansion and Scarborough Subway Expansion, are large, Progressive Design Build contracts opposed to fixed-price contracts for previous Ontario transit infrastructure projects Finch West and Eglington.

These projects will soon add an additional ~$6B to Aecon's backlog and will dilute fixed price contract exposure from 47% of ARE's current backlog to <25%, we anticipate this will incur in late 2024. This is down from >70% exposure to fixed contracts only a few years ago. In doing so, Aecon is much less likely to face material fixed-cost overruns and reduced profitability in the future, mitigating its risk profile, and substantially improved the quality and visibility of its underlying business.

Inflection in Business Quality & Returns on Capital

Beyond its proforma reduction to fixed-price contracts soon to be representing only ~25% of its backlog, Aecon is benefiting from both internal initiatives and broader industry trends that have yet to be appreciated by the market and highlight the disconnect between its current price and the quality of the business.

As we can see below, absent the cost overrides from ARE's four legacy fixed price mega contracts, the remainder of Aecon's business contributed margins >9% in 2023, compared to 4.5-5.5% EBITDA from 2015-2019.

Aecon's normalized margins have doubled from the pre pandemic era while Aecon also requires less invested capital to generate these earnings. We are modelling ~8% EBITDA margins for Aecon in 2024, well below the 9.2% margin we calculated in 2023.

With a three consecutive years of Aecon's reported results not reflected the normalized earnings power of the business, the market is also failing to appreciate Aecon's reduced invested capital required to generate these earnings.

Following the partial sale of the Bermuda airport, ARE's road tolling business and some non-core real estate, Aecon reduced its tangible and total capital by 21% and 49% respectively in 2023 while reported EBITDA was 60% below normalized EBITDA.

Going forward we conservatively model steady, ongoing annual increases in PP&E with perpetual Working Capital cash outflows, despite this we believe Aecon would produce well in excess of 40% Returns on Tangible Capital (EBIT/PP&E + Working Capital + Joint Ventures Invested Capital) based on operating margins of 6% in 2024 and improving by 30-40bps annually.

From a margin drivers perspective we believe this is both sustainable and visible when considering several factors:

Company-Specific Tailwinds

Positive mix shift away from fixed price contracts- these four contracts accounted for $215mn in loses in 2023 and $400mn cumulatively since 2021 a 50% reduction relative to $394mn in ARE reported EBITDA over the same 2021-2023 time period. At YE23 these contracts were down to 7% of Aecon's backlog or 5.5% assuming that ARE does not complete its remaining obligations on the Coastal GasLink project on which Aecon is seeking a legal settlement for shared-cost overrides. Arbitration is set for Q3/24.

Positive mix shift from asset divestment, Utilities growth- In May 2023 Aecon completed the divestment of its lower margin road tolling business for 8-9x TTM EBITDA receiving $235mn cash. The business was both capital intensive with capex at ~50% of EBITDA and working capital intensive with seasonal, outdoor work and hourly labor costs paired against a 90 day cash collection cycle. Aecon continues to experience accretive growth in its Utilities business with minority equity partner Oaktree investing $150mn in convertible preferred shares in October 2023 at an implied valuation of >9x TTM EBITDA. Oaktree is expected to further accelerate Aecon Utilities US pipeline. Three quarters of Aecon Utilities revenue is recurring, providing further margin visibility along with and no exposure to poor working capital from the lumpy milestone cash payments frequently associated with fixed-price contracts, helping to further reduce the invested capital required in the business. Utilities peers including MYR, Emcor, Mastec and Quantra trade for low to high teens EBITDA multiples.

Industry Tailwinds

Supply (competition) has continued to leave the E&C industry. Pre-pandemic Canada was at the forefront of the private-public partnership P3 model that popularized in the 2010-2015 time range and combined government-owned infrastructure projects with designs, building, construction and maintenance from the private sector. This attracted a wide range of US and International competitors into Canada RFP's. The industry competed aggressively for both the E&C- engineering and construction revenues within the same contract, absorbing the low margin, high risk revenues of the latter in order to secure the former. For example, ARE's large LRT Eglington contract was won in 2015 with only ~1/3rd of the design phase complete, much earlier in the process than typically necessary, in a highly competitive bidding process against 3 other consortiums with the acceptance of a fixed price contract being viewed as table stakes to enter the bidding.

Finding complex industries shifting from high supply to low supply tends to quickly lead to a positive step change in the underlying earnings power of remaining participants. This dynamic is further amplified by the nature case of the E&C industry .

Given the slow moving, multiyear project pipeline associated with the industry we believe the positive shift away from fixed-price contracts that began prior to the pandemic and was further accelerated by covid-induced supply chain shocks remains largely overlooked. Outside of Aecon we have seen margins inflect positively in the last ~18 months for Canadian peers AtkinsRealis and Stantec with multiples following suite as the industry collectively shifts away from fixed-price contracts.

Why? Beginning in the late 2010s and accelerated by covid- Canadian E&C's revenue has shifted collectively towards engineering, enabled by US+ International competitors largely leaving the domestic market. RFP's have gone from what was typically 4-5 bidders down to 2 which has led to higher recovery costs for both bidders. To elaborate- a large project will typically have upwards of $5 million in upfront costs associated with the bidding. Under the fixed price, legacy P3 environment this would lead $1-2 million in upfront revenue recovery for the winning bid and negligible cost offsets for the loser. In the current environment, these costs are almost all fully covered for the loser and fully baked into the successful bid by the winner. These leads to more favorable working capital dynamics with current costs relative to initial budget, reflected by faster cash collection from project launch until completion. As mentioned previously ARE is set to further benefit from reduced invested capital via the sale of its W/C intensive road tolling business in mid-2023.

With the shift to a less competitive steady-state industry and pandemic delays frequently representing a clause where E&Cs were not deemed solely at fault for delays outside of their control, contract negotiation leverage has now decidedly shifted in favor of E&C's against their public sector customers. Covid showcased that the industry was unable to handle exogenous supply chain shocks and accelerated the push by E&C firms for more downside protection from its customer base.

We're seeing this play out with the ongoing cost recovery for E&C's ex) Windsor Bridge Authority's recent payments to all 3 members of the Bridging North America consortium while Aecon has similar ongoing claims related to cost overruns for its two Toronto-based LRT projects and is currently awaiting binding arbitration for the Costal Gaslink project later this year.

Progressive design contracts act to effectively formalize the shared-risk dynamic that we are now seeing play out with ARE's legacy fixed-price contracts. The E&C provider will eat the margin impact of cost overruns up to a certain floor before they are partially reimbursed. The E&C while also benefit from performance payments with costs coming in below the projected budget. In doing so, there is shared up/downside risk with the customer and the probability of large write-downs is greatly diminished.

For Aecon this translates to >9% margins is the near-term being considered a base case while mid-single-digits (previously ARE's normalized margins from 2015-2019) should be considered the floor. We have seen repeated evidence of this play out with ~9% margin on >80% of Aecon's revenue in 2023, with legacy fixed-price projects down to ~5% of 2024 revenue this should become even more visible and undeniable for bears.

Fixed-price contracts will not go away entirely with ARE estimating ~25-30% of future revenue tied to fixed-prices, but with much smaller individual projects and the low likelihood of another pandemic followed by rapid inflation, downside risk should be much less likely and severe. As soon as ARE's two large Ontario-transit projects are formally recognized within backlog in the coming quarters we believe ARE will already surpass its desired 70-30% progressive build/fixed price revenue split on a pro-forma basis.

In summary Aecon has and continues to become a much better business over time where reported margins and FCF conversation should continue to trend higher while the risk of negative surprises trends lower. Accretive contribution margins paired with diminished working capital and minimal PP&E costs drives outsized returns on incremental capital going forward.

Today, Aecon's services are a collection of oligopoly business services with exposure to nuclear, utilities, industrials, chemicals and civil engineering. We expect Aecon to produce HSD/LDD margins, high returns on incremental capital with a customer base comprised of federal and provincial/state/municipal governments with multi-year project backlogs.

What's this worth? Certainly not ~3x NTM EBITDA.

Asymmetrical Investment Opportunity

The market is currently pricing Aecon with a trough multiple on trough EBITDA margins. Aecon has previously been acquired for an EBITDA multiple nearly TRIPLE its current value with margins HALF of what they are today. Aecon is a highly compelling opportunity given we see significant near term upside against very modest downside.

Aecon's current market cap:

With ARE taking project losses every quarter and repeatedly missing on earnings, investors have lost faith and Aecon’s shares have plummeted since the write-downs began in late 2021. ARE's sell-side analysts have mostly moved to hold or sell ratings with numerous downgrades, growing skepticism and consensus estimates modelling a permanent impairment in the profitability of the business. Consensus EBITDA margins in 2024 and 2025 at 5.2% and 6.1% respectively well below FY23's 9.2% normalized margins but up materially from consensus estimates of 4.8% and 5.4% prior to ARE's Q4 and FY23 results in early March which we believe highlighted how close Aecon is to completing its business transformation.

With the four impacted projects and associated write-downs approaching completion, we expect Aecon’s earnings to increase materially in 2024, revealing the true profitability of the business. Due to these outsized project losses, Aecon reported EBITDA margins of 3.1% in 2023, significantly below Aecon’s 4.5-5.5% long-term average. However, excluding these problem projects, Aecon’s core underlying business has achieved an all-time high EBITDA, with LTM margins of 9.2%. We believe Aecon should produce similar margins going forward for reasons we've listed previously and believe there is upside to our current revenue and margin estimates for 2024 and 2025.

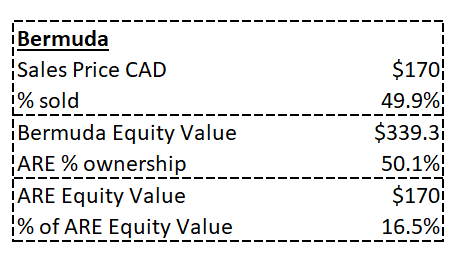

On a SOTP basis we can value Aecon based on two recent transactions. 1. Oaktree's minority investment in Aecon Utilities at a $750mn EV, $395mn equity value in October 2023 and 2. the partial of the Bermuda Airport in March 2023

Net of Utilities and Bermuda, Aecon remaining business is trading at 1.8x our 2024 EBITDA estimate:

Alternatively we believe that following Aecon's official addition of two large progressive-build Ontario-based transit projects to its backlog in 2H24, Aecon's backlog would represent its entire enterprise value based on an implied margin of 8.7%, 50bps below the normalized margins produced by Aecon in 2023.

Aecon's public sector services and E&C peers trade at mid-to-high teens EBITDA multiples relative to Aecon at 3.4x our 2024 EBITDA and 5.0x consensus. Aecon trades at a lower consensus multiple than Bird Construction, a pure-play construction company with 4% EBITDA margins.

This was epic. Thank you so much.

Have you looked into Duratec (AU)? Was pitched by Sohra Peak - similar multiple, smaller scale, more growth oriented than turnaround story