Tel Aviv Stock Exchange

High growth monopoly asset for 13x 2025 FCF

Tel Aviv Stock Exchange (TASE)

· High growth monopoly asset for 13x 2025 FCF.

Thesis:

· TASE operates a monopoly infrastructure asset growing revenue high-single-digits/low teens with high 20s operating margins, >70% incrementals and a series of accelerating share buybacks that has led FCFPS to compound at a 25% CAGR since TASE’s 2019 IPO.

· Despite its significant MOAT, durable growth, and exceptional returns on incremental capital; TASE is only trading for 13x our estimate of 2025 FCF net of cash or 16x EPS and 8x EBITDA.

· TASE's origins begin with a Visa-like existence which is only now in the final stage of its transformation to a publicly traded for-profit entity. The transition from a member owned, not-for-profit only began 2017 leading to an IPO in August 2019. It is rare in public markets to be able to purchase such a high-quality asset that is still so early its growth runway. Comparable financial infrastructure assets trade for 20-25x near term cash flows.

· TASE’s revenue streams are diverse, with non-transactional and transactional (trading) revenues accounting for 60% and 40% respectively, a split that is generally in line with global exchanges. TASE end-to-end solutions offering is unique among global exchanges and spans Israel’s entire capital markets infrastructure. Products and services include listing, trading in equities, fixed income, and derivatives, clearing and settlement, securities lending, IT/co-location, market data, and a growing indices business.

· TASE’s operating leverage provides high visibility on near- and long-term earnings power. TASE provides a significant disclosure around businesses costs by line item. We estimate ~80% of TASE's total costs are fixed.

· From 2017 to YE2023E, revenue has CAGR’d at 10% while total costs have grown 4% annually. Over the same time frame TASE Operating margins have TRIPLED, from 9% to 27%.

· Despite the increase, TASE margins remain well below those of more mature, for-profit exchanges. Comparable assets have produced 43-77% LTM EBIT margins. The biggest structural difference is these exchanges completed their demutualization processes 20 years prior to TASE, beginning in the late 90s (Australia 1998, NYSE 1999) followed by Toronto, London, Euronext, and CME in 2000, Mexico in 2001 and Brazil in 2007.

· As a public company, TASE has always run with a significant net cash balance sheet with upwards of 15% of its Enterprise Value in Cash. In mid-2022 TASE management began to actively return capital to shareholders via a series of increasingly large buybacks, 2023 YTD Shares Outstanding are down 8% y/y. In December 2023 TASE announced a 1-time special dividend payable in January 2014 for an implied dividend yield of ~11%. We believe TASE is an emerging share cannibal and will continue to deploy the majority of its FCF on share buybacks going forward.

· TASE also owns its real estate, a modern high rise building in downtown Tel Aviv, one of the most desired real estate markets in the world. We estimate net profits via a sale and leaseback transaction would represent ~25% of TASE’s current enterprise value.

Background

Historically, TASE operated as a member-owned, not-for-profit entity run primarily for the benefit of its shareholders, a consortium of Israeli banks.

Tel Aviv Stock Exchange (“TASE) origins date back to 1953 when a syndicate of Israeli banks and investment houses joined together to establish the exchange. In 1969 following the established of formalized Israeli Securities Law, TASE was granted a license to manage a domestic stock exchange and clearinghouse. Over time TASE would continue to expand its product offerings and technological capabilities in line with the world’s leading global stock exchanges. This included TASE establishing a clearinghouse to settle trades between buyers and sellers, launching electronic trading, derivatives and options trading, and exchange traded funds.

Despite its 70 year history, TASE’s current structure only dates back to only 2017. In 2017, the Knesset (Israel’s House of Representatives) approved an amendment for changes to TASE's ownership structure, paving the way for a process that is known as demutualization. Demutualization allowed TASE to become a for-profit business as a standalone entity owned by its shareholders opposed to its prior iteration as a not-for-profit collectively overseen, regulated and ran for the benefit of its members. In doing so TASE followed in the footsteps of notable securities exchange demutualizations including Stockholm (1993), Amsterdam (1997), Australia (1998), Toronto, London and the CME(2000) and the Chicago Board of Trade (2005).

Post demutualization in 2018, member of TASE’ legacy consortium announced the sale of 39% of TASE to a group of global, institutional investors for an aggregate value of ~$147 million USD (ILS $550mn). As part of the transaction 20% of TASE was sold to Manikay Partners, a long-term focused investment partnership with a heavy background in exchange-related demutualization transactions. Today, Manikay still owns its initial 20% along with a board seat. TASE’s second largest shareholder; The Novo Nordisk Foundation has increased its ownership to 8%, up from the 5% originally purchased as part of the 2018 transaction. Other notable TASE investors include Artisan Partners, Royce & Associates and Capital Group all of whom own >4.5% based on recent filings.

In July 2019, 66 years after its inception- TASE IPO’d 32% of its shares to foreign and Israeli investors at $7.10 ILS/share (ILS $225mn) with TASE legacy ownership consortium retaining the balance. The shares trade under “TASE” on the Tel Aviv Stock Exchange and can be found under TASE IT on Bloomberg. TASE is the only exchange in Israel.

Revenue

TASE revenue has grown by a 9% CAGR from 2017-2023E while operating margins have tripled from 9% to 27%. In Q4/22 management guided for a 10-12% revenue CAGR for 2023-2027 although 2023 YTD has been below target.

Transactional Revenue (~40%): These revenues are tied to the overall securities trading volume on TASE. Securities include equities, corporate bonds, structured bonds, convertible securities, ETFs and government bonds.

Non transactional Revenues (~60%) is split fairly evenly between Clearing House Services, Listing Fees and Data-Related revenue.

Clearing House Services: TASE’s Clearing House serves as a central counterparty for transactions executed as part of the trading on TASE. In doing so, the Clearing House is responsible for the risk that one of the parties will not complete its side of the transaction. TASE’s Clearing House also provides centralized custodian services for securities, this includes the execution of services for the payments of dividends, interest, redemptions, allocations of rights, bonus shares etc. TASE has a distinct clearing house that charges commissions for services related to the trading of derivatives called the MAOF Clearing House. Services are provided on a per fee basis while custodian fees are charged monthly based on asset values.

Listing fees & Levies: Listing and registration of securities. One-time fees on issuances and examinations plus annual fees which are charged based on market cap. Fees are collected up front, but revenue is recognized over time based on an estimate of the period in which the customer’s securities are listed on TASE, this helps drive negative working capital for TASE and leads to a “Deferred Income from Listing Fees” liability on TASE’s Balance Sheet.

Data distribution & connectivity: Real-time or delayed data offering to data distributors and financial institutions such as Bloomberg and Refinitive which are charged a monthly subscription fee for terminals, indices, data and connectivity services. Data-related revenues have grown at a double digit CAGR since 2017.

Organic growth drivers: TASE organic growth drivers stem from growth in Israeli GDP, more dual listed securities (market share gains), new products, higher volumes, and increased pricing. We believe embedded pricing power is one of TASE’s most unappreciated growth drivers. Given its not-for-profit origins, our work suggests TASE is currently under monetizing or simply not charging at all for numerous services. TASE Indices businesses is pricing at 15-20% of S&P and MSCI’s equivalent businesses while its derivatives business offers pricing that is >60% below that of other global exchanges. TASE must work in lockstep with the Israeli Securities Authority to determine future prices but has demonstrated an increasing ability to raise prices across select products and services in recent years.

New recent offerings from TASE include co-location services, pre-offering clearing services, a centralized lending pool, and cross-listing foreign ETFs. For example- co-location services provided by TASE was only launched in 2H2019. Co-location services includes hosting the clients’ servers at a TASE data center, providing a direct and faster connection to trading servers. Management has identified 100+ Israeli companies that are currently listed abroad with an aggregate market cap > $300B ILS as potential dual-listing candidates.

Unlike other businesses who must commit invested capital to find new customers and/or launch unproven products and services, TASE is simply following in the footsteps of older, more mature for-profit global exchanges against a highly visible cost profile, we believe this helps to de-risk under underwriting assumptions for TASE .

Operating Leverage

We are forecasting 27% Operating Margins for TASE in 2023 up from only 9% in 2017 and 23% in 2022. Since 2017, revenue has CAGR’d at 10% while total costs have grown at 4% annually.

Given the largely fixed cost nature of exchanges, TASE’s total cost base has increased at less than half the pace of revenue growth, having increased by <30% cumulatively from 2017-2023E.

Management

TASE is run by its CEO Ittai Ben-Zeev who joined the business in 2017 as it embarked on its demutualization process. Mr. Ben-Zeev came to TASE following an extensive career in capital markets both domestically and abroad.

In March 2023, TASE’s Board implemented a retention plan for Ben-Zeev, granting him 544,000 options at a strike price of $40 ILS per share, against what was a current share price of $16.50-$17 ILS and >100mn shares outstanding. The options do not vest for >5 years, becoming exercisable between June 1st 2028 and May 31st 2030. TASE shares must appreciate by almost 100% from its current price of ~$21.5 ILS. This was the Board’s second time providing such a package to the CEO, having granted 4.3mn warrants with a 5-year vesting period prior to TASE’s 2019 IPO. Similarly, the warrants required a 70% price increase from IPO with a $12.00 strike against a $7.10 listing pricing.

In February 2023, the board also approved a plan to issue warrants to additional members of the TASE’s C-suite. Approximately ~3mn warrants were granted to nine members of senior management with a $24.39 strike price vesting annually in equal amounts for three years beginning in February 2024.

In aggregate, Mr. Ben-Zeev, and the rest of TASE’s senior management team own more than 5% of the company. We believe this creates strong incentive alignment with shareholders and a focus on the long-term performance of the business.

Capital Allocation

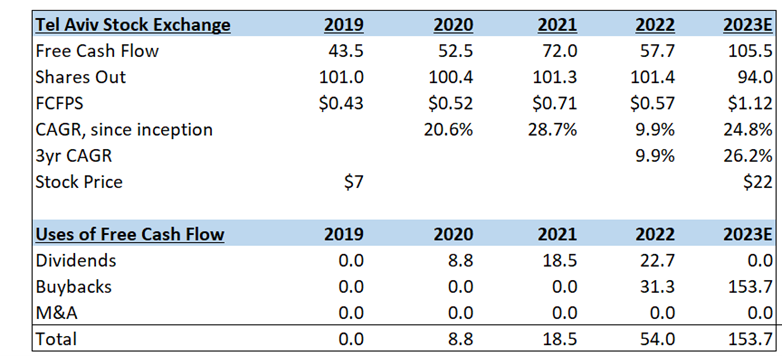

In mid-2022 TASE announced the cancelation of its regular dividend and initiated a share repurchase program beginning in May 2022 for up to $100mn ILS. In 2H2022 TASE spent $31mn ILS to repurchase ~2% of shares outstanding. In 1H2023 following share price weaknesses related to attempted judicial reforms by Israeli’s coalition government, TASE accelerated buybacks spending $131mn ILS to repurchase 7.7 million shares in 1H2023 including an $86mn SIB for 5% of the business from an existing shareholder. This was followed by an additional $21mn in Q3/23. Over 15 months from the initiation of the program in May 2022 until September 2023 (Q3/23) TASE has spent $185mn to repurchase over 9% of its shares at an implied average price that is a ~15% discount to the current share prices as of December 2023.

On December 14th, 2023 TASE pleased long time investors with an announcement that we believe will lead to a series of accelerated share repurchases and internal reinvestments back into the business.

Due to TASE’s demutualization history, TASE’s consortium of legacy pre-demutualization shareholders have remained subject to a unique provision that prevents the shares from being sold for a profit above the shares original cost basis of $5.08 ILS per share. This is strictly enforced by the Israeli Securities Authority, Israel’s equivalent to the SEC.

On December 14th, legacy shareholders agreed to divest 17.2m in remaining “Arrangement” shares in exchange for TASE paying out a one time $2.50 ILS/share dividend to ALL shareholders. The dividend was paid on January 2nd, 2024 to shareholders of record as of December 24th, 2023 and represents a $231mn cash outflow by TASE. On January 23rd, 2024 it was announced that all legacy shares had been sold in a secondary transaction at $20.60 ILS.

In return for the dividend payment, TASE will receive all profits from the 17.2mn shares in excess of the original $5.08 price. The shares were tio be divested over the next 12 months beginning on January 3rd 2024 prior to the updated announcement on January 23rd. TASE is not subject to a capital gains tax on these profits and will receive $242mn ILS after fees.

While the market may be reluctant to capitalize this non-recurring cash flow, the sale of Arrangement Shares does increase the already significant dry powder available to TASE, which we believe in turn is likely to be put towards continued share buybacks at attractive IRRs. We are modelling Free Cash Flow of ~$120mn in 2024 and ~$150mn in 2025 for TASE.

Hidden Asset-TASE HQ Real Estate

Upon the collection of Arrangement Share profits, TASE Enterprise Value will still embed one unique asset that we believe is being assigned zero value by the market, TASE 100% company owned headquarters in downtown Tel Aviv at 2 Ahuzat Bayit Street. The building is approximately 22,500 square meters spread across 14 floors.

Tel Aviv has been as hot as any real estate market in the world in recent years. Our understanding is that commercial rental space in in Tel Aviv's financial district is very hard to come by with rents beginning at ~$115-120 ILS/sqm and full-service equivalent rents in the range of ~$150-155 ILS/ sqm against cap rates in the range of 5.5-5.75%. Assuming $115 ILS/sqm and a very conservative 6.5% cap rate 2 Ahuzat Bayit is worth $475mn or ¼ of TASE’s current EV gross of tax. In 2019 TASE disclosed the depreciated cost of the property was $219m. We assume no material change and a 25% capital gains tax upon sale.

While our recent conversations with management suggest that nothing is imminent, TASE could monetize its HQ via a sale-leaseback or raise cash by taking out a mortgage on the building, which is currently debt free. As renters’ management believe it would need square meters for its 260 employees that is equivalent to annual rent of 2% of the price that the building would fetch in a sale.

Returns on Invested Capital

Given the operating leverage inherent in TASE’s business, we anticipate 2023 Net Income will have increased more than 4-fold from 2019. Now layer this against structurally negative working capital and a capex profile that has remained largely consistent on an absolute dollar basis and unsurprisingly TASE has shown to be a free cash flow machine with 25% FCFPS CAGR as a public company.

As discussed, TASE’s Capital Allocation has pivoted away from small dividends to large buybacks prior to the special dividend in January 2024. From 2019-2023E dividend payouts will have accounted for 15% of cumulative cash flow, 56% allocated to buybacks and the remainder has been retained by the business. Cash on hand has gone from $104mn ILS at YE19 to $230mn ILS as of Q3/23.

An additional FCF lever for TASE is that the business runs on negative working capital, which we believe is one of the most overlooked aspects of emerging compounder businesses. Most of TASE’s revenue is collected in cash on the date on which the corresponding service is provided, while payment terms are in the 30–90-day range for most major costs. This allows TASE to run its business on negative working capital, boosting FCF conversion above Net Income.

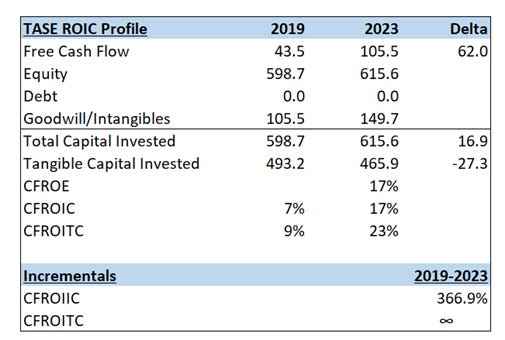

From 2019 to 2023 Total Invested Capital (We use Debt + Equity) has increased anemically at TASE. Our understanding is that TASE has never used Debt in its Capital Table while Equity has barely grown as Retained earnings, OCI and modest stock-based compensation have been largely offset by share buybacks. The biggest driver of growth in Invested Capital is related to TASE’s investments in Intangible technology and software assets related to new and existing products and services. When adjusting for these investments, TASE has incredibly removed tangible capital out of its business over time. As we can see below, TASE has nearly infinite returns on total incremental capital and tangible capital, a dynamic reserved for an incredibly select group of businesses.

Valuation

We believe TASE is trading at 13x 2025 FCF net of excess cash. Excess is TASE cash on hand less regulatory capital requirements and was $195mn ILS as of Q3/23 against reported cash on hand of $319mn ILS. This includes the $10mn net cash inflow we anticipate in 2024 related to the sale of Arrangement Shares by legacy shareholders less Q1/24’s one-time special dividend.

On an alternative basis if we were to value TASE purely based on its core business and without the imbedded value of its company-owned real estate, our cash flow multiple drops to 10x.